Are You Hedged?

Yes, I know. It’s been a while. We’ve been busy hedging. Are you hedged?

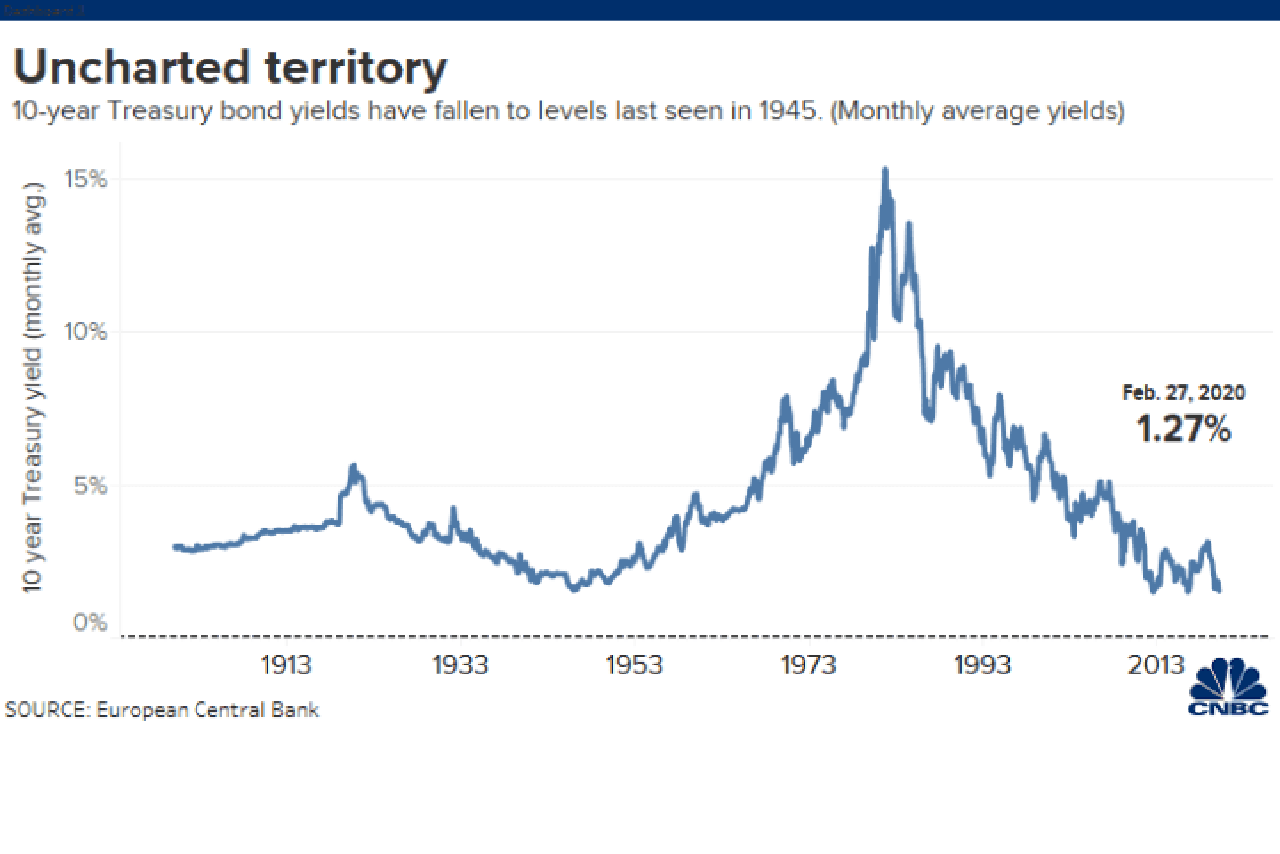

In recent months, bond market participants have been singing a very different song than stock market participants. Treasury yields have dropped significantly, nearing all-time lows (set in mid-2016), as institutional investors seeking safety have increased buying. Remember, when buying action in bonds drives the prices up, their yields move in the opposite direction. This safety seeking trend is indicative of perceived near-term economic weakness. But (somewhat isolated) stock prices have continued to rise in this time period, suggesting these participants think that consumption will continue growing near term. Much of this can be attributed to the theory that holds accommodative central bank (primarily the U.S. Federal Reserve) policy will support that continued consumption. So, as an individual investor, you might ask, which party is right? Where is the economy headed?

Every prognosticator is eventually right…

Let’s back up for a minute for yet another lesson and self-deprecating acknowledgement that I have been saying interest rates will rise for literally years now. Long enough for some, including our clients, to think Brendan is nuts. But as I’ve also said here before, every prognosticator is eventually right. And while the more we see, the more it seems rates could sink even further for longer, rates will go up at some point, and they could go up very sharply, and very quickly. Not because central banks want them to, but because the reality regarding the purchasing power of U.S. dollars (read real inflation), combined with a collective perception among lenders (mortgage lenders and bond buyers) that there is greater risk to lend, will eventually come home to roost. When lenders become fearful, they stop or reduce lending, which makes the cost of whatever they do lend go up. A lot.

Now back to our primary question. In which direction is the economy headed? North or south? Expansion or contraction? Incumbent politicians seeking re-election tell us the economy is the best it’s ever been, thanks to them, naturally. The prospective candidates for those political positions tell us the economy is terrible, that it’s a house of cards waiting for casual breeze.

What’s our answer to this cliff hanger? We don’t know. That may sound like a cop out, but it’s the truth. We don’t know what asset prices and interest rates are going to do in the near term because money is emotional. Even (especially perhaps) at the institutional level, fear and greed will drive the herd in either direction. And in a big hurry. Market and economic fundamentals flew out the window years ago, and speculation that central banks would continue “stimulating” the economy. But stimulus is, by nature, short lived. I’m no scientist, but I do know by instinct that stimuli lose efficacy the more of it you use, and the longer you apply it.

When the industry is collecting a percentage of your account value as their primary source of revenue, you can rest assured you will never hear them tell you to sell.

If you’re still reading, by now you’re thinking enough theory, what are you suggesting? Simply put, hedge your bets.

We have been conditioned by the financial institutions that we should keep all of our money in risk assets, primarily stocks, because if we don’t, we’ll get left behind. When was the last time you heard a money manager or financial advisor tell you to sell? When the industry is collecting a percentage of your account value as their primary source of revenue, you can rest assured you will never hear them tell you to. But now, more than ever, individual investors need to understand the real risk of staying “all in”. No individual investor can afford to be all in. Ever. But that’s what most investors are effectively advised to do. Now, the professionals I’m referring to would say they preach diversification too. But to justify and maintain their percentage fees, their diversifying hedge is a bond allocation. This will eventually backfire because with interest rates at all-time lows, bond prices are riskier than they’ve ever been, so keeping half of your money in bonds is not an effective hedge.

Central banks would never admit it openly, but the underlying message of their recent words suggests they are near capitulation. The experiment they’ve been conducting (more debt as a solution to a debt problem) has wearied them, and they are deeply concerned that the next time sentiment turns negative, their economic stimulation hammer will have run out of nails. They are calling upon politicians to exercise some fiscal discipline to relieve the pressure on them to carry the economy. And you don’t need a financial planner to understand the magnitude of that ask.

You’d all do well to take some time and gain a true understanding of your hedging strategy, if you are hedged. We can help.

Update: I wrote this post on Sunday, February 23rd. It’s now Friday, February 28th. Since then, unless you’ve been living in a cave, you know markets are in full panic mode over the corona virus. Global bond yields and stock prices are now plummeting together. What’s interesting about this to us is that this has been such a trigger. Fact: nobody knows what the real impact of this virus will be on the global economy. So, in that sense, market participants are overreacting. But in another sense, this drives home the fact that institutional investors have just been waiting for the straw that would break the camel’s back (RIP Ollie) and is a clear indication of just how over inflated prices were, and actually, still are. Ten percent in a week is obviously significant. But valuations are still two times higher than the historical mean and have only been this high two other times in modern history; before the crash that initiated the Great Depression in 1929, and before the dot com bubble burst in year 2000. What that means is, this could be just the beginning. I hope you’re hedged. If you aren’t, it’s not too late.

Written

February 28, 2020

Read Time

5 min read

More Posts